Transmission Infrastructure: Investment Models

Thought Leadership Series – Q1 2025

Propelling South Africa's Energy Transition through Investment in Transmission Infrastructure.

Author(s)

Mahlatsi Molokomme

Principal Investment Officer

Mpho Mokwele

Group Executive: Transacting

OVERVIEW

In October 2024, the National Transmission Company South Africa (NTCSA) unveiled its Transmission Development Plan (“TDP”) for the period 2025–2034, outlining the need to construct 14,500 km of new transmission lines and 133,000 MVA of transformer capacity over the next decade. This requires an estimated R440 billion in investment.

This infrastructure expansion is a pre-requisite to integrating new renewable energy generation capacity i.e. 56,000 MW of new generation capacity anticipated between 2025 and 2034. The current construction capacity of about 800 km of transmission lines per year needs to increase significantly to an average of 1,450 km per year, with the potential to peak at around 2,700 km annually.

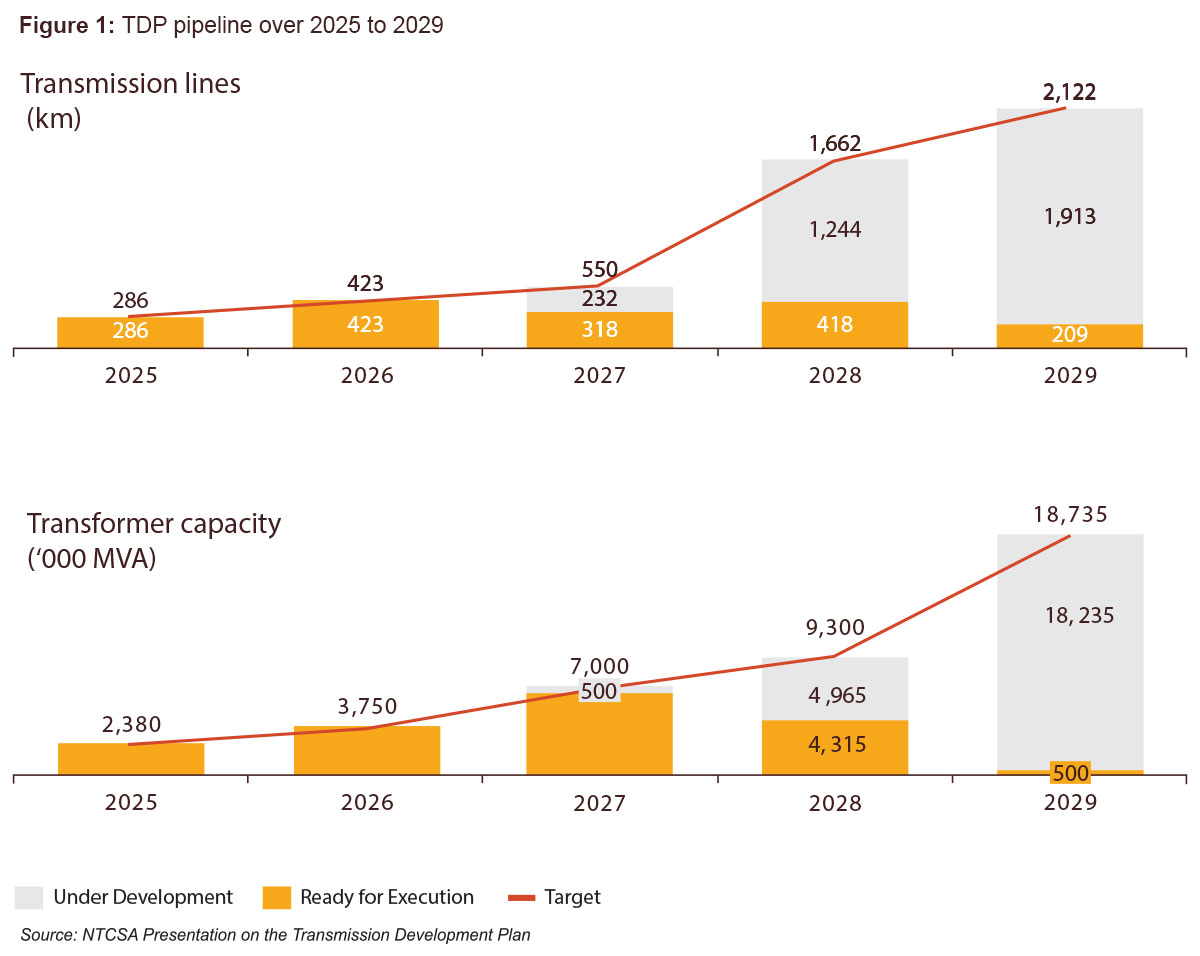

The TDP pipeline over the next five years comprises of projects that are either ready for execution or in various stages of development (total 5,000 km). This first phase rollout will require an investment amount R112 billion between 2025 and 2029.

To complement the efforts towards the expansion of the grid, the Ministry of Electricity and Energy (“MoEE”), in collaboration with the National Treasury, launched a Request for Information (“RFI”) on 12 December 2024, as a pathway to implementing the pilot project under the Independent Transmission Projects (ITP) programme. This initiative seeks to gather insights from private developers, financiers, and other stakeholders to inform the ITP pilot planned for launch in November 2025, covering the procurement of 1,164 km of transmission lines from private investors.

Given the speed and scale required to implement the TDP in the context of the public funding constraints, the ITP is designed to enable off-balance sheet financing for transmission infrastructure and ultimately mobilise private capital towards bridging the investment gap.

All ITP models are based on the private party undertaking construction and financing risk with variations regarding ownership, operational and maintenance obligations. ITPs have worked well in attracting private investment in transmission lines for emerging economies such as India, Brazil, Peru and Chile. These models, typically using build-operate-transfer (BOT) contracts, have enabled the construction of nearly 100,000 km of new transmission lines and mobilised over USD24.5 billion in private capital between 1998 and 2015. The ITPs introduced transparent, competitive bidding processes for transmission projects such that, in Peru, the model resulted in cost efficiencies where winning bids were 36% lower than anticipated.

TRANSMISSION INFRASTRUCTURE INVESTMENT MODELS

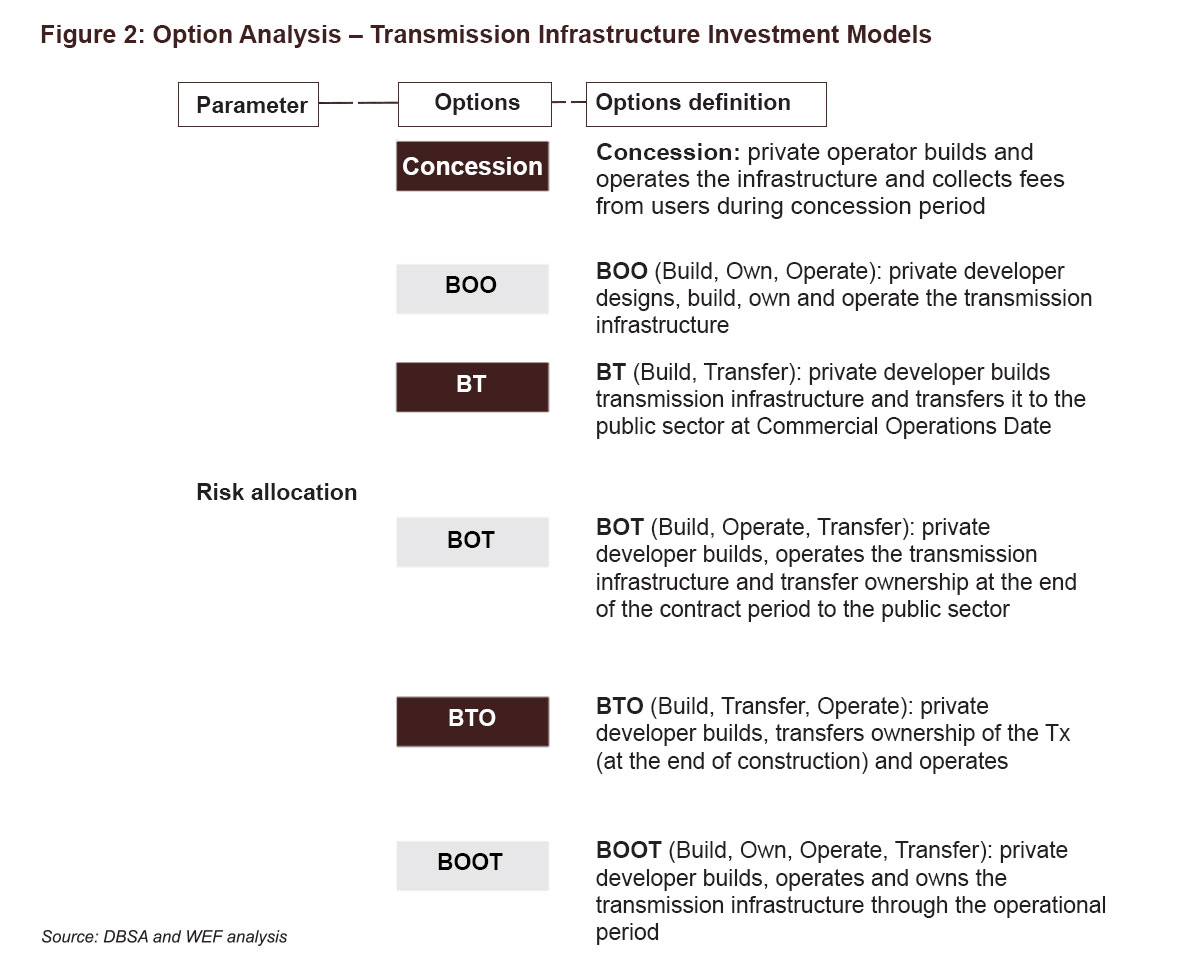

Under the Mobilizing Investment in Clean Energy (“MICE”) initiative, the DBSA and the World Economic Forum conducted a comprehensive market sounding in the first half of 2024 on the various transmission investment models that can be implemented. This exercise evaluated various investment models to determine the most suitable approaches for South Africa's transmission infrastructure needs. Key consideration was given to factors such as financial viability, risk allocation, and alignment with national energy objectives. The following transmission investment models were considered:

- Concessions: In this model, the private party builds and operates the transmission infrastructure and collects fees from users during the concession period.

- Build-Own-Operate (BOO) Model: In this model, a private developer builds, owns, and operates the transmission infrastructure. While effective in countries like Chile and India, it can be contentious due to private ownership of transmission which is essentially public infrastructure.

- Build-Own-Operate-Transfer (BOOT) Model: In this model, a private developer builds, owns, and operates the transmission infrastructure during the operational period and transfers the ownership to the public utility (such as the NTCSA[1]) at the end of the contract period. This model has been successful in Peru, India and Brazil.

- Build-Transfer-Operate (BTO) Model: In this model, ownership transfers to the public utility immediately after construction, when commercial operations begin. This model has been used effectively for toll roads in South Africa, demonstrating its bankability.

A key consideration in relation to deriving bankable transmission investment models from the perspective of government is the ownership of the transmission network by the private sector.

Based on the market sounding exercise we conducted, Concessions and BTO transmission investments models are preferred for implementing large scale ITPs as they maintain public ownership and control of the transmission infrastructure. The BT model (as described below) could be considered for small-scale projects, as it allows for quicker financing and execution than public built projects but still maintain public ownership.

BANKABILITY OF INDEPENDENT TRANSMISSION PROJECT(S)

There is currently no country in Africa that has successfully implemented pure ITP networks. However, the widespread adoption of Independent Power Producer (IPP) models across the continent establishes a strong precedent for private sector participation in the energy sector. Given the comparable risk profiles of IPPs and ITPs, ITPs have the potential to follow a similar trajectory, provided the necessary regulatory, financial, and structural enablers are in place.

In infrastructure finance, bankability refers to the extent to which a project is considered financially viable and attractive to investors and lenders. A bankable project must demonstrate a stable revenue model, predictable cash flows, manageable risks, and a clear regulatory framework that ensures investors can achieve a reasonable return on investment.

Ensuring the bankability of ITPs requires addressing investor concerns regarding procurement models, tariffs, and risk allocation:

| Key Factor | Mitigation Strategies |

| Procurement Models | Transparent and competitive bidding processes, similar to the Renewable Energy Independent Power Producers (“REIPP”) Programme, will be important for attracting private investment. |

Tariff Structure | Ensuring that use-of-system tariffs are cost-reflective is equally important for lenders, investors and the public utility (NTCSA). The National Energy Regulator of South Africa (“NERSA”), as the independent regulator, will need to expedite the necessary tariff reforms to establish predictable income streams for transmission projects. |

| Revenue Certainty | In the absence of a strong balance sheet from the off-taker (“NTCSA”), the establishment of ring-fenced revenue accounts could provide lenders with the requisite security and assurance over the project's income streams, reducing liquidity risks. |

| Performance-Based Payment Structures | Payment structures that are linked to the availability and performance of the transmission infrastructure would incentivise private operators to ensure the reliable operation and maintenance of the assets, reducing demand risk for investors. |

| Risk Allocation | Transmission infrastructure projects inherently carry significant risks, including land acquisition, right-of-way, and construction-related challenges. The government (NTCSA and the Department of Public Works and Infrastructure) are best positioned to handle land acquisition or right-of-way risk. |

| Credit Enhancements | To ensure that transmission investments models are bankable, they must be underpinned by appropriate credit enhancement mechanisms. The World Bank is currently assisting the National Treasury in developing a credit guarantee vehicle as an alternative to government guarantees. |

CONCLUSION

Collaboration between government, DFIs, and the private sector will be key in unlocking the R440 billion investment needed to strengthen the country's transmission network. The DBSA's holistic approach to infrastructure investment—from project preparation to financing and implementation support—positions it as a key enabler in propelling the country's energy transition.

By establishing a clear regulatory framework, streamlining procurement processes, and providing the necessary risk mitigation tools, South Africa can create an enabling environment that attracts private capital and accelerates the delivery of the TDP.

Download here Propelling South Africa's Energy Transition through Investment in Transmission Infrastructure